GreatAsic: Designing Malaysia’s Next Chip

🌎 Issue #102

It’s Tuesday, and today we’re discussing GreatAsic, a Malaysian chip design company. Founded in 2024 by Ong Chin Hu and Michael Liew Woon Chin, the company just raised a $6.9 million Pre-Series A round led by Vertex Ventures Southeast Asia & India, with participation from Ehsan Kapital and Gobi Partners.

The Context

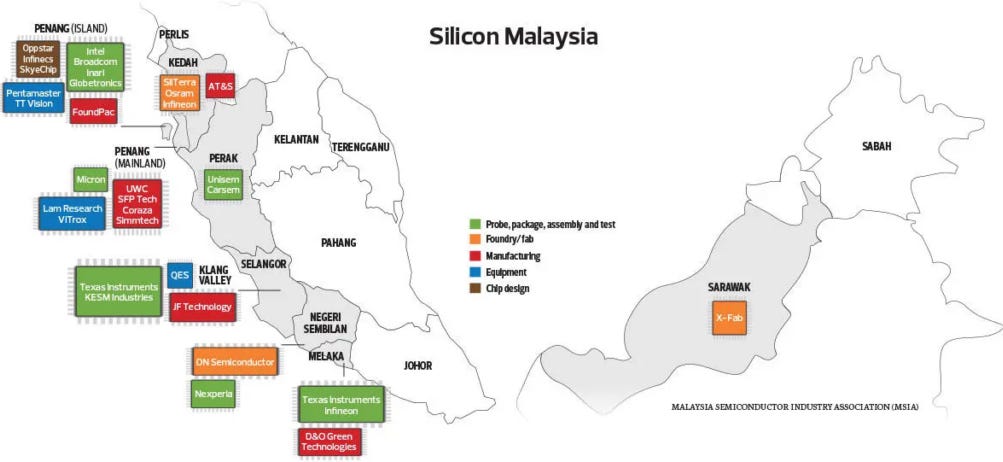

Malaysia has long been a semiconductor hub, especially in what one might call “back-end” activities: assembly, packaging, and testing. That said, there are some front-end specialty fabs and a lot of supporting industrial electronics. The country is the sixth largest semiconductor exporter, has a 13% share of the global packaging market, and the industry contributes 40% to Malaysia’s total exports.

While semiconductor packaging is more high-tech than most industries, it’s less advanced compared to other parts of the value chain. To that end, outsourced semiconductor assembly and test (OSAT) contributes just 6% of the global value, while fabrication adds 24%, and semiconductor design and software add another 50%. To move up the value chain, the country introduced a 10-year National Semiconductor Strategy in 2024.

For our purposes, three core points of the strategy matter:

The government plans roughly ~$6 billion in incentives, infrastructure, financing, and industry support, and wants to attract over $100 billion in investments overall.

A core goal is to develop local semiconductor champions, and not just attract foreign investment.

Malaysia aims to train 60,000 semiconductor engineers and technicians and reduce talent leakage to other industries and countries.

Before we get to one of the first measures the government executed, and one that is key to our story, I should note two broader tailwinds that help explain why Malaysia made this move now.

First, of course, is the AI boom. Since 2023, Microsoft, Nvidia, Google, and ByteDance have announced billions of dollars of investment in Malaysia, mostly in cloud services and data centers. There would be no better time to capture some share of global investment into the industry than now.

Second is diversification. Malaysia is less exposed than China or Taiwan to the US-China chip conflict, and the country is positioned to benefit from Chinese companies diversifying assembly outside China. In addition, Germany’s Infineon and America’s Intel expanding existing facilities and building new advanced packaging capacity. While this is still the assembly part of the chain, it brings in investment that strengthens the broader industry by supporting talent training, creating additional government revenue, and so on.

{kind=link}

Now, while Malaysia has some real strength in the industry, it is extensively reliant on foreign actors for capital. 97% of investment in the electronics industry as a whole comes in the form of foreign direct investment. Hence, it’s hard to call the industry sovereign, which increases the risk of capital flight. And since Malaysia’s real economy is heavily dependent on semiconductors, that capital exodus would be devastating.

If Malaysia wants to move up the value chain in the monetary sense of the phrase, it either needs to enter the fabrication step or the design step. Creating a TSMC-like company is nearly impossible, which leaves design as the more viable option. There are other segments to target, particularly semiconductor equipment manufacturing, but capital requirements are substantial there as well, and most categories are dominated by a single player.

Which brings us to the measure I mentioned a couple of paragraphs ago.

Malaysia agreed to pay $250 million to Arm in an agreement that gives local companies access to Arm IP, high-end chip design blueprints, and training for 10,000 engineers. The program has two tiers: AFA for startups and smaller chip companies, and CSS for larger firms developing advanced processors for AI, cloud, and data centers. Malaysia received 25 AFA and seven CSS licenses under a 10-year agreement1.

Arm is also opening its first Southeast Asian office in Kuala Lumpur. The end goal is for the country to create 10 local chip producers, with each bringing in $1.5-2 billion in revenue.

The company that was one of the first three to receive access to Arm’s blueprints is GreatAsic.

The Product

GreatAsic was not only the recipient of the blueprints, but actually was the only company that got access to both AFA and CSS tokens. Those are the base layer for the company to build its offering.

If you are non-technical like me, the easiest way to understand the products behind GreatAsic is to first look at what the company actually does, and then go into the products.

As a System-on-Chip (SoC) provider, GreatAsic goes through the following process to deliver its products:

Front-end design: this is where the company works through the chip’s architecture, understands the power-performance trade-offs, selects the IP, and so on. It’s the first step in turning the customer’s vision into a scalable solution.

Physical design: if front-end design says what the chip should do, physical design decides how that logic is implemented on a chip so it can be manufactured.

Testability design: after the chip is made, it needs to be tested. That logic also needs to be decided before the manufacturing process. It makes the chip easier to inspect, debug, and produce in volume.

FPGA prototyping and emulation: these are two types of tests GreatAsic runs before manufacturing begins. FPGA prototyping means taking a reprogrammable integrated circuit, testing part of the chip’s logic on it, and checking whether it behaves correctly. Emulation is another way of testing a chip, but on large hardware machines like this one.

In reality, there are many more steps in the process, but I think we can get enough of an understanding of what the business does just by looking at those four.

The end result of the process is the actual SoC. It’s a chip designed for specific use cases. It combines several parts of a computer system. Put another way, if we oversimplify things, you can have a CPU, GPU, and networking as separate components, or you can build everything onto one chip.

Because everything is integrated, the device is smaller, uses less power, and costs less at scale than a system built from separate chips. The downside is that there’s less flexibility in what the chip can do.

Beyond SoCs, GreatAsic offers semiconductor IP cores. IP cores are reusable chip components. So instead of designing every part of a chip from zero, a company can use pre-built blocks and combine them into a full chip.

The company also builds software solutions for chips. Which is fairly simple: if there’s no software, the hardware can’t be used.

The Business Model

GreatAsic engages with clients on a project basis. The company follows one of three approaches:

ASIC Turnkey, where it takes full responsibility for the project and leads it from end to end. The customer defines what the chip needs to do, while GreatAsic executes the path from design to chip output.

ASIC Co-development, where it works with the client’s team to bring the desired design to life.

Customized IP Design, where it works on the IP, while further SoC development happens on the client’s side. I’m speculating here, but two paths may exist: IP can be bundled into customer projects or sold as custom IP work.

While SoCs are custom chips, there are still reusable parts, like the aforementioned IP or automation tools. That means GreatAsic doesn’t really start every project from scratch, and it has reusable components. That should improve delivery speed and margins.

The company mentions that its SoCs could be used in data centers, edge AI, IoT, automotive, and consumer electronics. All of these industries are mostly controlled by large enterprises. On the one hand, those are the clients you want to target: they are more inclined to engage in large long-term deals, they have a growing need for chips, and one client can make the business. On the other hand, most chip design companies want to target the largest enterprises, which leads us to…

The Bear Case

As long-time readers know, I don’t like using competition as a bear case argument, but there is a lot of competition in this space. There are both specialized vendors (Qualcomm, MediaTek) and integrated players (Apple, Google) competing here. And I don’t think that, at this point, GreatAsic has done a great job explaining how it differentiates itself from large or even medium-sized players.

With such broad positioning, it would be hard to convince the largest enterprises to choose your product when there are proven alternatives on the market. The national story does sound nice, but I don’t think that alone sells.

I feel like the biggest risk is just getting the business off the ground and capturing those first customers. That’s true with many businesses, but it feels especially true in the semiconductor space.

The Bull Case

But maybe the fact that this is a young company doesn’t matter that much because demand is so high. We hear a lot about the chip shortage at the highest level of the stack, with your OpenAIs and Anthropics, but there are thousands of other potential customers who want to participate in the AI boom. It could be an enterprise with an on-premise data center that wants to create a testing ground for deploying internal AI applications. It could also be a startup training domain-specific models that doesn’t want to entirely rely on hyperscalers.

Additionally, the unfair advantage that GreatAsic has, and American companies don’t, is that the US government won’t be backstopping up-and-coming chip design startups in the same way. And I think Malaysia could. If GreatAsic isn’t where it wants to be in a couple of years, I can see a universe where the government provides funding in the form of direct stimulus, a grant, or even becomes a core customer.

The Takeaway

What’s the one lesson investors and founders can take away from GreatAsic?

While investors want to give a chance to young entrepreneurs, and many young entrepreneurs have an unwavering belief in themselves, there’s value in experience. Case in point, GreatAsic. Both founders have extensive experience in the industry. And I’m dubious that, were they not as experienced, they would get the same level of non-VC support.

1: AFA (Arm Flexible Access) gives startups and smaller companies access to Arm’s chip design library without large upfront licensing fees. CSS (Arm Compute Subsystems) provides larger companies with pre-built chip components, allowing them to develop chips faster instead of designing everything from scratch